Cash Flow Crisis Management: The 72-Hour Triage Playbook

Key Takeaways

- 60% of small businesses struggle with cash flow in 2025

- 82% of business failures stem from cash flow — not profitability

- Automation can cut billing errors by up to 60%

- A 90-day forecasting habit is your strongest defense

- Late payments, rising costs, and margin compression are the three hidden killers to watch

60%

of small businesses struggle with cash flow in 2025

U.S. Bank

82%

of business failures trace back to cash flow — not profitability

SCORE

60%

reduction in billing errors after automation

Intuit

30 days

target DSO for healthy small business cash conversion

SBA

In the relentless landscape of 2025, small and mid-sized business leaders are grappling with unprecedented financial pressures. Industries like professional services, retail/e-commerce, manufacturing, tech startups, and healthcare are particularly vulnerable, where cash flow management for small businesses has become the make-or-break factor for survival. With inflation lingering and economic uncertainties persisting, around 60% of small businesses struggle with managing their cash flow, leading to stalled growth, payroll strains, and even closures. Understanding your overall business health is the first step to breaking free. This isn't just a statistic—it's a reality for busy leaders juggling operations while seeking quick, high-ROI solutions to small business financial challenges.

At BizHealth.ai, we act as your Business Health Coach, delivering AI-driven diagnostics across 12 key areas like Financials, Operations, and Strategy to eliminate guesswork and uncover efficiencies. Our platform empowers you to turn business cash flow 2025 obstacles into sustainable growth levers, yielding 20-25x ROI on affordable assessments. If you're earlier in the journey, our small business survival checklist covers the year-one fundamentals every owner should pressure-test before scaling. In this comprehensive guide, we'll dissect the cash flow crisis, explore digital strategies, identify hidden killers, provide a proactive framework, and discuss when to leverage AI tools over traditional experts. Let's shift from crisis mode to confident scaling—stop guessing, start growing.

Am I in a Cash-Flow Crisis? — Quick Self-Check

If two or more of these apply to your business right now, your cash flow needs immediate attention:

- Payroll stress — You've delayed, borrowed, or scrambled to make payroll in the last 90 days

- Rising receivables — Your accounts receivable balance is growing faster than your revenue

- Shrinking reserves — Your cash buffer has dropped below two months of operating expenses

- Margin compression — Your costs are rising faster than you can raise prices

- Vendor pressure — You're stretching payables, getting late-payment notices, or losing early-pay discounts

- Delayed owner pay — You've skipped or reduced your own compensation to keep the business running

Checked two or more? Read on for the framework — or jump straight to the below.

Understanding Cash Flow: The Lifeblood of Your Business in 2025

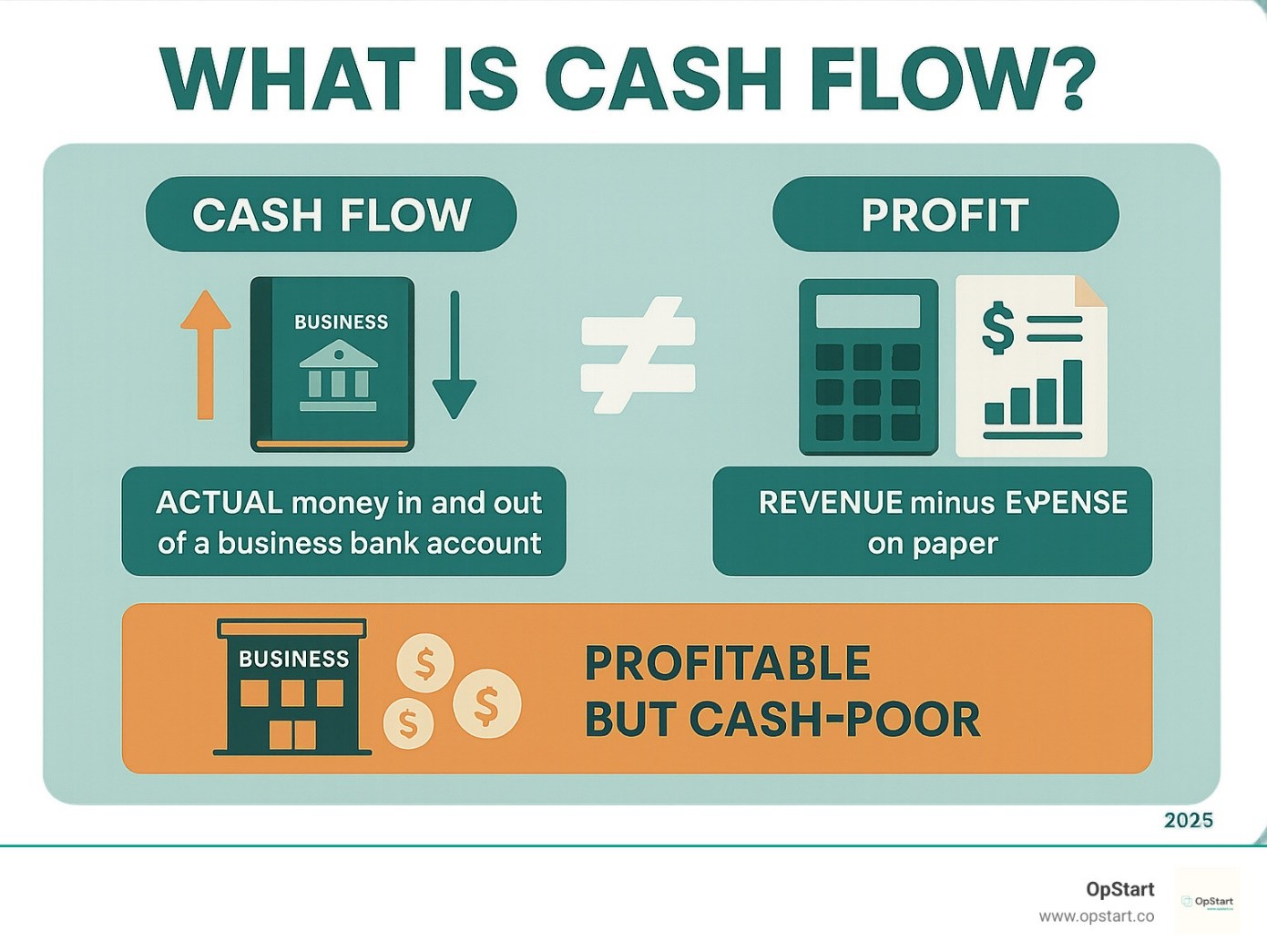

Source: opstart.co

Cash flow represents the actual money moving in and out of your business bank account—not just revenue minus expenses on paper. A profitable business can still be cash-poor if payments are delayed or expenses come due before revenue arrives. This distinction is critical in 2025's high-inflation environment where timing matters more than ever. Getting a clear picture of your financial position starts with understanding where you stand today — here's how to check your business health across all 12 key areas.

The 2025 Cash Flow Reality: Why Traditional Spreadsheet Management Is Failing Small Businesses

As we navigate 2025, the cash flow reality for small businesses is stark: traditional methods like manual spreadsheets are no longer sufficient amid high-inflation pressures. The U.S. Small Business Administration (SBA) reports that 70% of small businesses face cash flow constraints, exacerbated by inflation as the top macro challenge. In high-inflation environments—where costs for labor, supplies, and energy have surged—spreadsheets fall short because they lack real-time insights and predictive capabilities. For a deeper look at the forces reshaping finances this year, see our breakdown of small business financial trends in 2025.

Critical Insight:

82% of business failures stem from poor cash flow management, not lack of profitability. This disconnect is amplified in global markets like the UK (5.45M small businesses with 90% optimism but volatile post-Brexit costs) and Canada (58% growth but regulatory burdens), where English-speaking hubs mirror U.S. challenges.

Why are spreadsheets failing? They rely on historical data, ignoring dynamic factors like delayed payments (affecting 51% of small businesses) or unexpected spikes in supplier costs. In 2025, with B2B SaaS markets hitting $300B and 53% AI adoption for efficiency, small businesses clinging to outdated tools risk margin erosion and liquidity crunches.

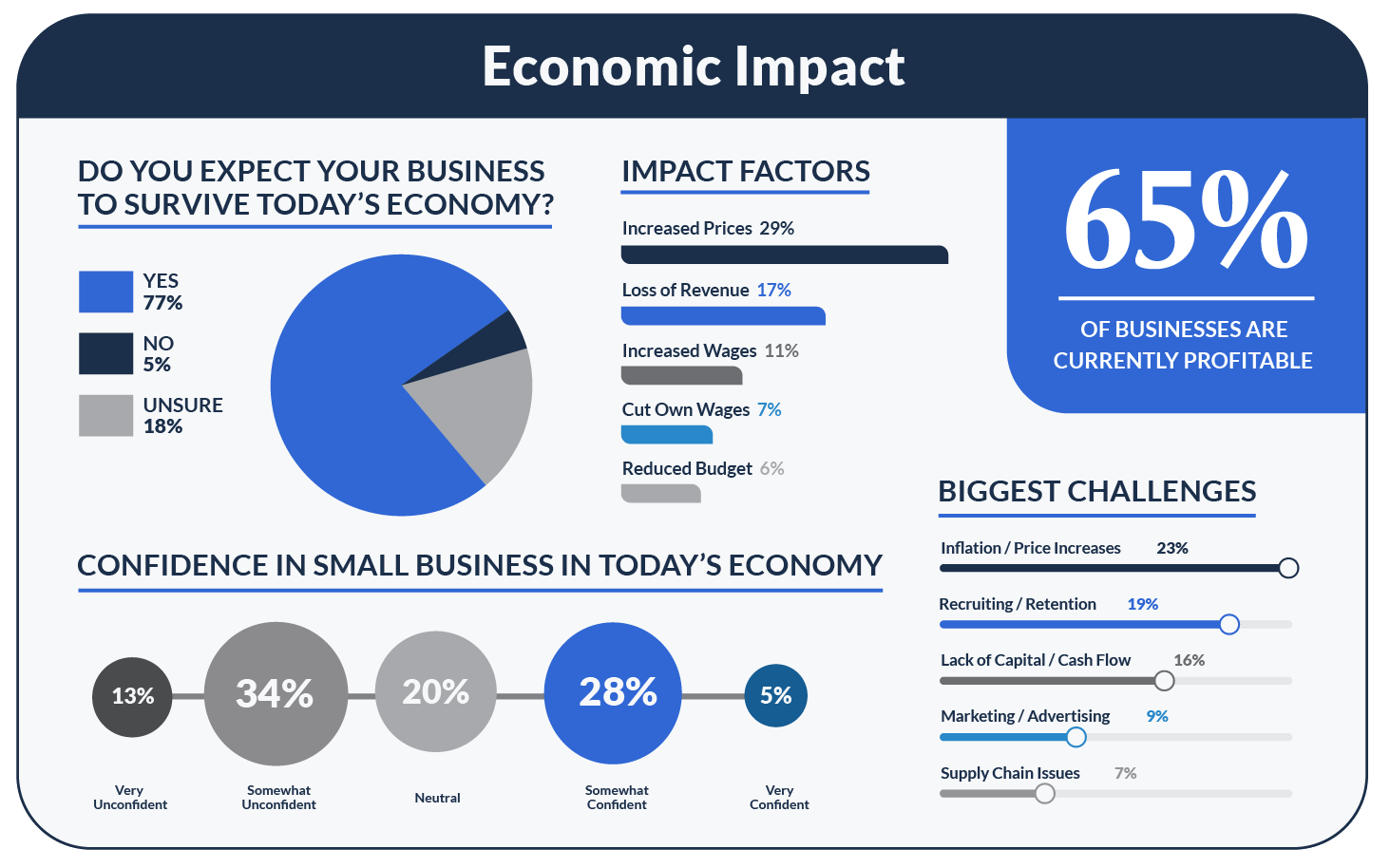

Source: re2.ai - Small Business Statistics 2025

Key 2025 Statistics:

- •77% of businesses are currently profitable, yet many face cash flow pressures

- •23% cite inflation/price increases as their biggest challenge

- •19% struggle with recruiting/retention, impacting operational efficiency

- •9% identify lack of capital/cash flow as a primary obstacle

- •47% feel unconfident or very unconfident about surviving today's economy

Cash Flow Check

Is money leaking from your business right now?

60% of small businesses struggle with cash flow—but most don't know exactly where the leaks are. A 45-minute assessment pinpoints the gaps before they become a crisis.

No consultants. No ongoing fees. Just clarity.

Digital Transformation Strategies: How Automation Reduces Billing Errors by 58.7%

Digital transformation is no longer optional—it's essential for mastering business cash flow 2025. Automation tools streamline processes, reducing billing errors by up to 60-80% and accelerating collections, per industry reports. For small businesses, this means shifting from error-prone manual invoicing (which delays payments and ties up capital) to AI-driven systems that flag discrepancies in real-time.

Key Digital Strategies:

1. Automated Invoicing and Reminders

Tools like HubSpot or QuickBooks integrate with CRMs to send invoices instantly, cutting days sales outstanding (DSO) by 30-50%. This addresses late payments, a top cash killer affecting 45% of U.S. small business owners who forego paychecks due to shortages. Before investing in a CRM, read our CRM reality check for small businesses to make sure it fits your stage and needs.

2. Predictive Analytics for Forecasting

AI platforms analyze patterns to predict cash gaps, enabling proactive adjustments. Gartner notes two-thirds of small businesses plan AI investments for efficiency, yielding 15-25% gains.

3. Integrated Payment Gateways

Embed options like Stripe for instant collections, reducing errors and boosting liquidity. In e-commerce, this offsets inventory cash ties and improves working capital management.

Globally, these strategies adapt well: In Singapore (300K+ small businesses with 20-25% efficiency gains via AI), or India (62.5M MSMEs), automation levels the field against inflation. For BizHealth.ai users, our diagnostics auto-recommend solutions from Financials gaps to BizGrowth courses, fostering 30%+ transitions and 20-25x ROI.

Framework for Systematic Cash Flow Assessment: From Reactive to Proactive

Shift to proactive cash flow management with this systematic framework that moves you from firefighting to forecasting:

Maria runs a 15-person e-commerce fulfillment company in Denver. Revenue hit $3.2M last year — her best year yet. But by February, she couldn't make payroll without pulling from her line of credit. The problem wasn't sales. Two major clients had shifted to net-60 payment terms, her warehouse lease had jumped 18%, and she'd invested $140K in inventory for a Q1 product launch that underperformed. On paper, the business was profitable. In the bank account, she was eight days from a crisis.

Maria's story isn't unusual — it's the pattern we see in the majority of small businesses that come to BizHealth.ai for a financial health check. The framework below is what helped her get from reactive to proactive in 13 weeks.

Source: jaroeducation.com - Top 10 Financial Management Tips

1Assess Current State

Calculate key metrics—cash conversion cycle, DSO, operating cash flow. Knowing your financial numbers inside and out is non-negotiable. Not sure which numbers matter most? Start with these financial health metrics every small business owner should track. Use dashboards or AI tools to track performance — for a ready-made system, explore the fractional CFO toolkit: 7 financial dashboards built for small business visibility. Aim for 60-90 day inventory turns to optimize working capital.

Key Metrics Explained

| Metric | What It Means | Warning Sign | What to Do Next |

|---|---|---|---|

| Days Sales Outstanding (DSO) | Average number of days it takes to collect payment after a sale | Over 45 days, or trending upward for two consecutive months | Tighten payment terms to net-15 or net-30, automate invoice reminders, and follow up on overdue accounts within 48 hours |

| Cash Conversion Cycle (CCC) | Total days between paying for inventory/inputs and receiving cash from customers | Longer than your industry average, or lengthening quarter over quarter | Shorten receivable terms, negotiate longer payable terms with suppliers, and reduce inventory holding time |

| Operating Cash Flow (OCF) | Cash generated by your core business operations after paying operating expenses | Negative for two or more consecutive months while the business is nominally profitable | Identify the gap between paper profit and actual cash — common culprits are uncollected receivables, prepaid expenses, and inventory buildup |

| Gross Margin Trend | Percentage of revenue remaining after direct costs (materials, labor, production) | Declining for three or more months, or falling below your industry benchmark | Audit your cost of goods sold line by line, renegotiate supplier contracts, and evaluate whether your pricing reflects current input costs |

Days Sales Outstanding (DSO)

What it means: Average number of days it takes to collect payment after a sale

Warning sign: Over 45 days, or trending upward for two consecutive months

What to do: Tighten payment terms to net-15 or net-30, automate invoice reminders, and follow up on overdue accounts within 48 hours

Cash Conversion Cycle (CCC)

What it means: Total days between paying for inventory/inputs and receiving cash from customers

Warning sign: Longer than your industry average, or lengthening quarter over quarter

What to do: Shorten receivable terms, negotiate longer payable terms with suppliers, and reduce inventory holding time

Operating Cash Flow (OCF)

What it means: Cash generated by your core business operations after paying operating expenses

Warning sign: Negative for two or more consecutive months while the business is nominally profitable

What to do: Identify the gap between paper profit and actual cash — common culprits are uncollected receivables, prepaid expenses, and inventory buildup

Gross Margin Trend

What it means: Percentage of revenue remaining after direct costs (materials, labor, production)

Warning sign: Declining for three or more months, or falling below your industry benchmark

What to do: Audit your cost of goods sold line by line, renegotiate supplier contracts, and evaluate whether your pricing reflects current input costs

2Forecast Future Flows

Use predictive AI for 90-day projections, factoring in seasonality and market trends. Industry data shows 20-25% efficiency uplifts from proper forecasting tools.

Your 13-Week Cash Triage Plan

The 13-week cash flow view is the standard crisis-planning format used by turnaround advisors and CFOs. It forces weekly granularity — close enough to act on, far enough out to plan. Here's a triage-ready action plan you can start this week:

| Week | Focus Area | Key Actions |

|---|---|---|

| 1 | Emergency visibility | List every cash inflow and outflow expected over the next 13 weeks. Open a dedicated tracking spreadsheet or tool. Record your current cash balance as your baseline. |

| 2 | Receivables triage | Identify every overdue invoice. Contact each customer with a specific payment date request. Offer a small early-payment discount (1–2%) on large outstanding balances if it accelerates collection. |

| 3 | Payables negotiation | Rank vendors by urgency (payroll taxes and rent first, discretionary last). Contact non-critical vendors to request 15–30 day extensions. Identify any early-pay discounts you're missing. |

| 4 | Expense audit | Review every recurring charge. Cancel or pause anything non-essential. Renegotiate contracts where possible — many SaaS tools, insurance policies, and service agreements have flexibility if you ask. |

| 5 | Pricing review | Compare your current pricing to your actual cost of delivery. If margins have compressed, model a 5–10% price increase on your most price-inelastic offerings. Test with new customers first. |

| 6 | Revenue acceleration | Identify your fastest path to new cash: pre-sell a service package, offer a discount for upfront annual payment, launch a limited-time bundle, or invoice milestone payments on in-progress work. |

| 7 | Forecast reconciliation | Compare actual cash movement from weeks 1–6 against your week-1 forecast. Adjust the remaining 7 weeks based on what you've learned. Flag any shortfall weeks. |

| 8 | Credit & financing review | If a gap remains after operational fixes, evaluate options: business line of credit, invoice factoring, SBA microloan, or equipment financing. Apply early — don't wait until you're desperate. |

| 9 | Process automation | Implement at least one automation: auto-invoicing, payment reminders, recurring billing, or expense approval workflows. Even one automation frees up hours and reduces errors. |

| 10 | Inventory & WIP optimization | If you carry inventory or work-in-progress, identify slow-moving stock or stalled projects tying up cash. Liquidate, discount, or complete them to convert back to cash. |

| 11 | Customer pipeline review | Assess your sales pipeline for revenue timing. Push to close any deals that are decision-ready. Shorten proposal-to-signature cycles. Focus on repeat customers — they convert faster. |

| 12 | Buffer building | With 12 weeks of data, calculate your true minimum cash need. Begin routing any surplus into a dedicated reserve account. Target one month of operating expenses as your first milestone. |

| 13 | Systemize & repeat | Document what worked. Set up a recurring weekly 30-minute cash review. Build this 13-week view into your permanent operating rhythm — not just a crisis tool. |

List every cash inflow and outflow expected over the next 13 weeks. Open a dedicated tracking spreadsheet or tool. Record your current cash balance as your baseline.

Identify every overdue invoice. Contact each customer with a specific payment date request. Offer a small early-payment discount (1–2%) on large outstanding balances if it accelerates collection.

Rank vendors by urgency (payroll taxes and rent first, discretionary last). Contact non-critical vendors to request 15–30 day extensions. Identify any early-pay discounts you're missing.

Review every recurring charge. Cancel or pause anything non-essential. Renegotiate contracts where possible — many SaaS tools, insurance policies, and service agreements have flexibility if you ask.

Compare your current pricing to your actual cost of delivery. If margins have compressed, model a 5–10% price increase on your most price-inelastic offerings. Test with new customers first.

Identify your fastest path to new cash: pre-sell a service package, offer a discount for upfront annual payment, launch a limited-time bundle, or invoice milestone payments on in-progress work.

Compare actual cash movement from weeks 1–6 against your week-1 forecast. Adjust the remaining 7 weeks based on what you've learned. Flag any shortfall weeks.

If a gap remains after operational fixes, evaluate options: business line of credit, invoice factoring, SBA microloan, or equipment financing. Apply early — don't wait until you're desperate.

Implement at least one automation: auto-invoicing, payment reminders, recurring billing, or expense approval workflows. Even one automation frees up hours and reduces errors.

If you carry inventory or work-in-progress, identify slow-moving stock or stalled projects tying up cash. Liquidate, discount, or complete them to convert back to cash.

Assess your sales pipeline for revenue timing. Push to close any deals that are decision-ready. Shorten proposal-to-signature cycles. Focus on repeat customers — they convert faster.

With 12 weeks of data, calculate your true minimum cash need. Begin routing any surplus into a dedicated reserve account. Target one month of operating expenses as your first milestone.

Document what worked. Set up a recurring weekly 30-minute cash review. Build this 13-week view into your permanent operating rhythm — not just a crisis tool.

This plan is a starting framework — adapt the timing and actions to your business model. The critical habit is the weekly cadence: 30 minutes every Monday reviewing your cash position keeps small problems from becoming crises.

3Implement Controls

Automate payment reminders, diversify revenue streams (e.g., add subscriptions), and build cash buffers—target 3-6 months of operating expenses as a safety net.

4Monitor and Adjust

Conduct quarterly reviews and integrate insights with operations for agility. This proactive approach boosts resilience and prevents crisis situations.

When to Seek Expert Help vs. Leveraging AI-Powered Diagnostic Tools

Know when to escalate: If cash crunches persist despite implementing basics, traditional consultants offer deep dives but at $10K+ costs with uncertain outcomes. Instead, leverage AI for unbiased, data-driven insights. Start with a free financial health check to see where your numbers stand before deciding on your next step.

The BizHealth.ai Advantage

Our $199-$799 assessments deliver comprehensive reports in under 90 minutes, addressing small business financial challenges with actionable insights that drive 15-20% efficiency gains.

- ✓20-25x ROI on affordable assessments

- ✓AI-driven diagnostics across 12 key business areas

- ✓Personalized recommendations with 30%+ success transitions

- ✓Direct links to ecosystem solutions like BizGrowth courses

When to use AI: Routine diagnostics, cash flow analysis, operational efficiency assessments, and strategic planning—areas where data-driven insights excel.

When to seek experts: Complex restructurings, legal matters, major pivots, or situations requiring specialized industry knowledge and hands-on implementation.

Conclusion: Stop Guessing, Start Growing

In 2025, cash flow crises threaten 60% of small businesses, but with digital transformation strategies, identification of hidden killers, and proactive forecasting frameworks, you can not only survive but thrive. The key is moving from reactive firefighting to data-driven decision making — what we call moving from impact over information. If you're a leader who suspects deeper issues beyond cash flow, our breakdown of the most common leadership blind spots will help you pinpoint root causes. And when you're ready to translate insight into action, our tiered diagnostic plans starting at $199 deliver a full 12-area assessment in under 90 minutes. For a broader look at what a complete assessment covers, read our complete guide to business health assessment. For comprehensive guidance on building better financial systems, explore our financial management resources for small businesses.

BizHealth.ai empowers small business leaders with AI-driven diagnostics that eliminate guesswork and uncover hidden efficiencies. Our platform transforms cash flow obstacles into sustainable growth levers, delivering measurable ROI and actionable insights you can implement today.

Frequently Asked Questions About Small Business Cash Flow

Your Next Step

Ready to Stop Guessing and Start Growing?

Begin growing your business today with a comprehensive business health assessment. Your growth starts here.

Assessments from $199 · Results in under 90 minutes

Further reading: Explore common accounts receivable mistakes that strangle cash for a deeper look at this connected topic.

Further reading: Explore sharks circling when a business hits crisis for a deeper look at this connected topic.

Built for home services: Home Services Cash Flow Guide

Related Articles

Explore more insights to help grow your business

The Fractional CFO Toolkit: 7 Financial Dashboards Every Small Business Needs

Build the financial visibility system that fractional CFOs use to transform small business performance.

Stress-Test Your Pricing: A Framework for Margins and Cash Flow

Learn how to evaluate and optimize your pricing strategy to protect margins and improve cash flow.

Financial Health Metrics Every Business Owner Should Track

Master the key financial indicators that predict business success and sustainability.

About the BizHealth.ai Research Team

The BizHealth.ai Research & Analysis Team combines over five decades of hands-on experience in business ownership, executive leadership, management consulting, and strategic advisory. Our team has guided hundreds of small businesses through financial challenges, operational scaling, and growth planning — bringing real-world expertise to every assessment and resource we publish. All content is reviewed for accuracy against current industry data, SBA benchmarks, and recognized frameworks including the McKinsey 7S Model and Balanced Scorecard methodology.

Learn more about our approach →Related reading: Most cash flow crises trace back to running the business out of one undifferentiated financial bucket.